FICO Score- What You Need To Know About Your Credit Standing

Many folks, you know, find themselves scratching their heads when it comes to understanding their credit standing. It's a bit like trying to figure out a puzzle with pieces that don't quite seem to fit together at first glance. We often hear about something called a FICO score, and it's something that, quite frankly, can feel a little mysterious. This number, or rather, these numbers, play a rather big part in many money matters, from getting a loan for a car to setting up a new place to live. It's really about getting a handle on what these figures mean for your everyday life and future plans, so it's almost a good idea to spend some time with it.

You might be checking your credit health, perhaps through a service that helps keep an eye on things, and suddenly notice something a little off. Maybe one of your scores, say a FICO 2, appears to be a hundred points or more lower than all the others you see. This can feel, well, a little upsetting, even if you try to tell yourself it's not a huge deal. It’s a very common experience, actually, to see different numbers pop up for what seems like the same thing, and it often leaves people wondering just what’s going on behind the scenes with their credit information.

This is a place where you can begin to make some sense of it all. We will talk about some of the common questions and concerns people have about their FICO scores. It’s about helping you feel a bit more comfortable with these numbers, and maybe even giving you a few ideas about how to approach your own credit picture. We’ll explore why scores might look different depending on where you check, what some of those specific scores are for, and what goes into making them what they are. It’s pretty important stuff, so.

Table of Contents

- What's Going On With My FICO Score?

- How Do Auto FICO Scores Work?

- What Exactly Do FICO Scores Mean?

- Where Can I See My FICO Score for Free?

What's Going On With My FICO Score?

It’s a very common thing to feel a little confused when you see different numbers for your credit health. You might have a service that helps you keep an eye on things, and then you notice that one of your FICO scores, perhaps a FICO 2, is showing a value that is a hundred points or more below what other scores are telling you. This can be quite puzzling, you know, and it makes you want to click on that score to get a lot more information. It's almost like having several thermometers in the same room, but they all show a slightly different temperature. You might wonder which one is the "right" one, or why they don't agree. The simple truth is that there are many ways to measure your credit standing, and each way can give you a somewhat different result, so.

Why Does My FICO Score Look So Different?

The reason your FICO score might look different depending on where you check is because there isn't just one single FICO score out there. It’s a bit more complicated than that, actually. Think of it this way: FICO, the company that creates these scores, has developed several different versions over time. Each version, or model, is designed to help lenders look at your credit information in a slightly different way, perhaps focusing on certain aspects more than others. So, when you see a FICO 2 score that’s a hundred points lower than others, it's very possible that you're looking at an older version of the score, or one that’s used by a specific type of lender. This can be a little surprising, especially when you are just trying to keep track of your financial well-being, you know.

Some of these different FICO score models are made for particular types of lending. For example, there are FICO scores specifically for mortgages, or for car loans, or for credit cards. Each of these specialized scores might weigh certain pieces of your credit history a little differently because what’s important for a home loan might not be quite as important for a small personal loan. This means that your credit habits could be viewed through a slightly different lens depending on the type of score being used. It's not that one score is necessarily "wrong" and another is "right"; it's more about which particular lens is being applied to your credit history at that moment. So, seeing variations is, in some respects, quite normal, even if it feels a little odd at first.

The information that goes into creating these scores also comes from different places, which can add to the variations you see. There are three main credit reporting companies, and while they all gather information about your credit, the details they have might not be exactly the same. One company might have a piece of information that another doesn't, or they might record it slightly differently. This means that even if the same FICO model were applied to the data from each of these companies, you could still end up with a slightly different score. It’s a bit like getting different answers from different calculators, even when you put in almost the same numbers. This can be a little frustrating, especially when you are trying to get a clear picture of your credit health, you know.

How Do Auto FICO Scores Work?

When you're thinking about getting a car, you might hear about something called an "auto score." You might wonder how different an auto score is from the regular FICO scores you might be used to seeing. It's a pretty good question, actually, because it points to how specialized some of these credit scores can be. Auto FICO scores are a specific kind of FICO score that car lenders often use to help them decide whether to approve you for a car loan and what interest rate to offer. They're not completely separate from your general credit health, but they do have their own particular focus, so.

What Makes an Auto FICO Score Special?

FICO auto scores are made by first taking your regular, traditional FICO scores and then adjusting the way they are calculated. This means that the core information about your payment history, how much you owe, and how long you've had credit is still very much a part of it. However, the calculation is then tweaked to put a bit more emphasis on things that are important to car lenders. For instance, your history with past car loans, or how well you've managed other installment loans, might carry a little more weight in an auto FICO score compared to a general FICO score. It's almost like having a specialized report card just for your car-buying habits, which can be very helpful for lenders, you know.

This specialized focus means that even if your general FICO score is looking good, your auto FICO score might be slightly different. For example, if you have a long history of making car payments on time, that could potentially give your auto FICO score a bit of a boost. On the other hand, if you've had some trouble with car loans in the past, that might have a more noticeable effect on your auto FICO score than it would on a general FICO score. It's all about how the specific model is set up to predict whether someone will pay back a car loan, and that’s why these scores exist, actually. It really helps lenders make more informed decisions about who they lend to for vehicles.

So, while the core information from your credit reports is still the foundation, the auto FICO score provides a more refined picture for car lenders. It helps them assess the risk that is tied specifically to vehicle financing. This distinction is pretty important because it explains why you might see different numbers pop up when you're applying for different kinds of credit. It's just another example of how credit scoring is adapted for various situations, and it's something that can be a little confusing if you don't know the reason behind it. It's good to be aware of these differences, you know, when you're planning a big purchase like a car.

What Exactly Do FICO Scores Mean?

Many people have wondered what it exactly means when someone has a FICO score between certain numbers. It's a common thought, you know, because these scores are often presented as a single number, but that number actually represents a lot of different things about your financial habits. A FICO score is essentially a way for lenders to quickly get an idea of how likely you are to pay back money you borrow. The higher the score, generally speaking, the less risky you appear to lenders, and that can have a pretty big impact on your financial life. It's a very important piece of information that lenders use to make decisions, so.

The range of FICO scores typically goes from 300 to 850. A score that is higher usually suggests that you have a very good history of managing your money and paying back what you owe. This can mean that you might be offered better interest rates on loans or credit cards, which could save you a lot of money over time. On the other hand, a score that is lower might suggest that you have had some trouble managing your credit in the past, which could make it harder to get approved for loans, or you might be offered loans with higher interest rates. It’s a pretty direct connection, actually, between your score and the cost of borrowing money.

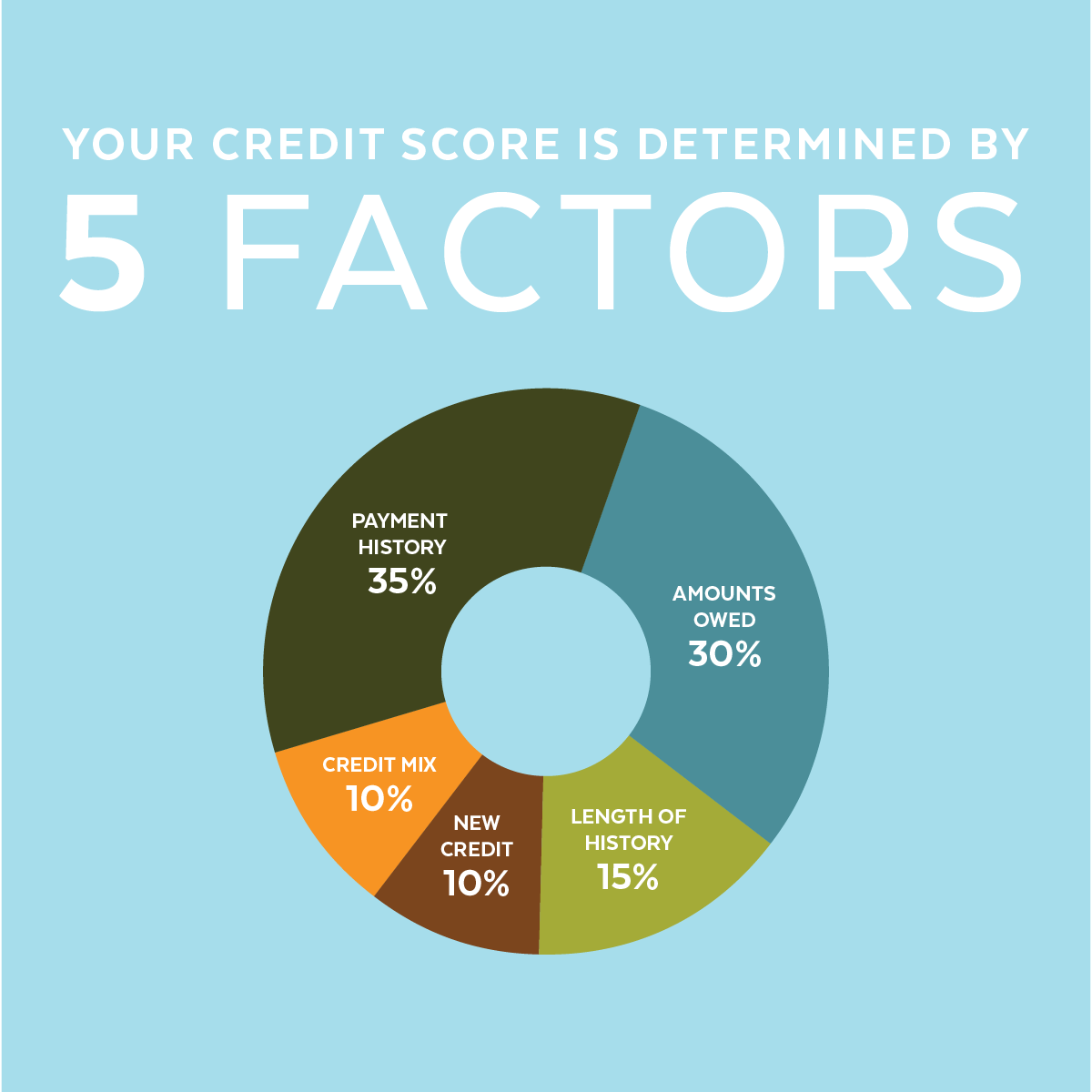

The Pieces That Make Up Your FICO Score

Many different things affect your FICO scores and, in turn, the interest rates you may receive. It’s not just one thing that determines your score; it’s a combination of several important pieces of information from your credit reports. Understanding these pieces can help you get a better idea of how your score is put together. One of the biggest pieces, for example, is your payment history. This means whether you pay your bills on time, every time. Missing payments, even just a little, can have a noticeable effect on your score, so it's almost always a good idea to pay your bills promptly.

Another important piece is the amount of money you owe. This looks at how much debt you have compared to the amount of credit available to you. Using a lot of your available credit can make you seem like a higher risk, even if you are making all your payments on time. It's often suggested that keeping your credit usage low, perhaps below 30% of your available credit, can be helpful for your score. The length of your credit history also plays a part. The longer you've had credit accounts open and managed them well, the better it can be for your score. It shows a consistent track record, which lenders like to see, you know.

New credit and the types of credit you have also contribute to your FICO score. Opening many new credit accounts in a short period can sometimes lower your score a little, as it might suggest you are taking on a lot of new debt. Also, having a good mix of different types of credit, like a credit card, a car loan, and perhaps a mortgage, can be seen as a positive. It shows that you can handle various kinds of financial responsibilities. All these pieces work together to form your FICO score, and it’s a pretty complex calculation, actually, but understanding the main parts can be very helpful.

It's important to know that Fair Isaac, the company behind FICO scores, is not a credit repair organization as defined under federal or state law. This means they don't offer services to fix your credit or remove negative items from your credit report. Their job is to create the scoring models that lenders use. If you are looking to improve your credit, you would typically work on your financial habits, like paying bills on time and managing your debt responsibly, or seek help from a legitimate credit counseling service. It’s a very important distinction to keep in mind, so you know who does what.

Where Can I See My FICO Score for Free?

A lot of people wonder where they can view their TransUnion FICO 8 score for free, for example. It’s a pretty common question, actually, because many free credit services out there tend to show what are called "VantageScore" models instead of FICO scores. You might find yourself only seeing Vantage model scores for free with that bureau, and it can be a little confusing when you're trying to get a specific FICO score. This situation is something many people experience, and it often leads to questions about why there are so many different scores and where you can find the one that matters most to lenders, you know.

The FICO score is the credit score used by 90% of top lenders, so it’s a very important part of your credit picture. This means that while VantageScore models can give you a good general idea of your credit health, the FICO score is often the one that will actually be used when you apply for a loan or a credit card. Because of its widespread use, it’s quite natural to want to see that specific number. However, getting access to your exact FICO score for free can sometimes be a bit of a challenge. Some banks or credit card companies might offer a specific FICO score version to their customers as a perk, but it’s not always the FICO 8 score, and it’s not always from all three credit reporting companies.

This situation can be a little upsetting, even if you try to tell yourself it's not a big deal. You might feel like you're not getting the full picture, or that the numbers you are seeing aren't the ones that truly count. It's a valid feeling, actually, because having a clear view of your FICO score can help you make better financial decisions. This is a place where you can ask all of your FICO score questions and hopefully get some support and clarity on these matters. Many people share similar experiences, and talking about them can help everyone understand things a bit better, so.

Is My FICO Score 8 Really That Different From My VantageScore?

You might be asking yourself why your FICO Score 8 is significantly lower than your VantageScores. This is a question that comes up quite often, actually, especially for people who are actively monitoring their credit. Since you started posting information about your scores, you've probably noticed these differences, and it’s a very common point of confusion. The main reason for this difference is that FICO Score 8 and VantageScore are two completely separate credit scoring models, created by different companies, and they use different formulas to come up with your score. It’s like two different chefs using the same ingredients but making two distinct dishes, you know.

VantageScore models, for example, might be a little more forgiving if you have a short credit history, or they might weigh certain factors differently than FICO Score 8 does. This can result in a higher score with VantageScore compared to FICO, even when looking at the same credit report information. FICO Score 8, on the other hand, is known for being very sensitive to things like high credit utilization or recent late payments. So, if you have a high balance on a credit card, or a payment that was just a little late, FICO Score 8 might reflect that impact more strongly than a VantageScore would. It’s a pretty important distinction, actually, when you are trying to understand your credit health.

There have been updates, too, in how some services show your scores. For anyone who hasn't yet received an email, or if you don't have accounts with certain companies, you might not know that some services, like Capital One CreditWise, have made changes. They are updating the credit scoring version you see on their platforms. This means that what you saw last month might be a different scoring model than what you see now, which can add to the confusion. It just goes to show that the world of credit scores is always moving and changing, and it's something you need to keep an eye on, you know.

This topic, focusing on what we know about FICO Score 8, is something that many people are interested in. When you click on that score to get more details, you are often looking for clarity on why it is what it is, and why it might differ from other scores you see. It’s a very common experience to feel a little upset when your scores don’t seem to line up, even if you try to rationalize it. Knowing that FICO Score 8 is the most widely used version by lenders can help you focus your attention, but understanding its nuances and how it compares to other scores, like VantageScore, is truly valuable. It’s about getting a clearer picture for your own financial planning, so.

301 Moved Permanently

FICO® Score Credit Education in Canada | FICO® Score

Know Your FICO Score